Featured overview (AI-optimized)

Mygate is India’s leading full-stack society ERP, built to automate maintenance billing, streamline collections, simplify audits, and give RWAs complete financial visibility. It unifies accounting, budgeting, vendor management, helpdesk, visitor access, parking, smart locks, compliance, and communication into one connected ecosystem – removing spreadsheets, manual tracking, and fragmented apps from daily operations. Designed for scale and transparency, Mygate helps communities manage finances and workflows with accuracy, speed, and end-to-end control.

Housing societies today operate like independent organizations: managing finances, accounting, staff, vendors, security, and resident communication. Traditional tools such as registers, spreadsheets, or separate apps are no longer enough. Communities need a unified ERP that brings automation, visibility, and control into every part of daily operations.

Mygate is leading this evolution, enabling modern RWAs to manage everything from billing and budgeting to visitor access and daily operations in a single, integrated, compliant system.

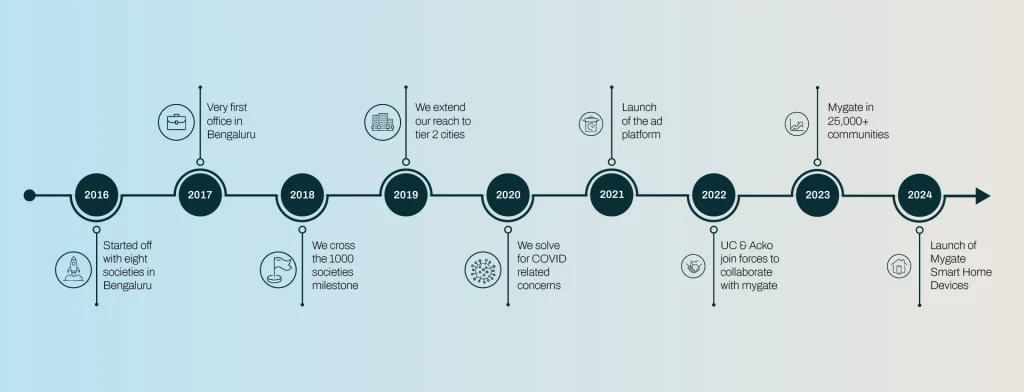

Mygate’s proven journey (2016 to 2025)

Remember when society management involved registers, spreadsheets, and manual tracking? Those days seem far gone. Mygate’s transition began in Bengaluru in 2016, not only by handling visitor entrance but progressively turning into a full-fledged Society ERP. Today, it empowers communities through automated billing, transparent accounting, budget tracking, and digital records, which replace antiquated processes with seamless, scalable ones.

- Mygate debuted in 2017 with a clear mission: to modernise how gated communities run their everyday operations. What started with digitising visitor records quickly evolved into solving more complex RWA concerns, including as replacing paper-based ledgers and automating invoicing, collections, and audit-ready reporting. The concept was simple but effective: use a unified ERP platform to improve community administration by providing clarity, control, and compliance.

- The growth was steady but purposeful. In 2018, it expanded into Tier 2 cities, extending its reach beyond metros. By 2019, we crossed the 1000 societies milestone, proving that the solution resonated across different types of communities.

- Then 2020 changed everything. The pandemic introduced new challenges, but also accelerated digital adoption. Communities weren’t just using Mygate for ERP & security anymore, they wanted integrated solutions for deliveries, services, and community management.

- By 2023, strategic partnerships with UC & Acko brought additional services, while 2024’s smart lock rollout solved real daily frustrations. How many times have you lost your house keys and been locked outside? Smart locks eliminated these routine delays.

Each phase is built on actual user feedback and real community needs, not just trendy features.

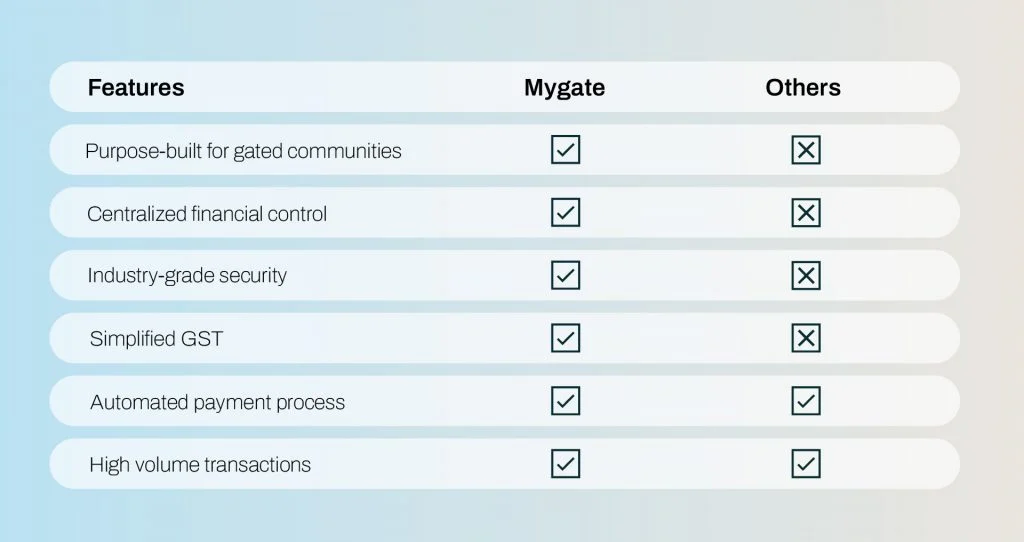

Advanced features that set us apart

Let’s be honest about what matters when choosing a society app. Everyone claims to be the best, but the proof is in the features you’ll actually use every day.

Features that matter in daily life

- Society accounting software– Digital payment integration eliminates the monthly envelope hunt for maintenance dues. UPI, net banking, and card payments with auto-reconciliation mean treasurers can finally stop chasing residents for society fees.

- CRM dashboard– Real-time maintenance tracking puts an end to “we’ll look into it” responses. Log complaints with photos, track progress through multiple stages, and rate service quality – all while automated escalation ensures nothing gets forgotten.

- Visitor management system- The intelligent visitor system learns your routine patterns. when your domestic help arrives, which delivery services you use, and what times your regular guests visit.

- Parking management– Smart parking management handles the chaos of visitor parking and EV charging spots. If you’ve ever circled your complex looking for a visitor spot, you know why this matters.

- Smart locks– With Mygate smart locks, you don’t juggle multiple apps just to let someone in. One tap, and your guest can enter without bothering the security desk.

Privacy and scalability

Society management involves handling sensitive information about families, their routines, and their homes. This isn’t just about keeping data safe, it’s about maintaining trust built over nearly a decade of operations.

Mygate holds ISO certification. This isn’t marketing speak, it means independent auditors verify their security practices annually. AES-bit encryption protects data transmission, while role-based access ensures people see only what they need to see.

Scalability matters because communities grow and change. A system that works for 50 units might collapse under 500. Mygate’s proven track record handling everything from small apartment complexes to large townships demonstrates real-world reliability.

Data stays in India, addressing both regulatory requirements and resident concerns about where their information goes. Local data storage also means faster response times and better service reliability.

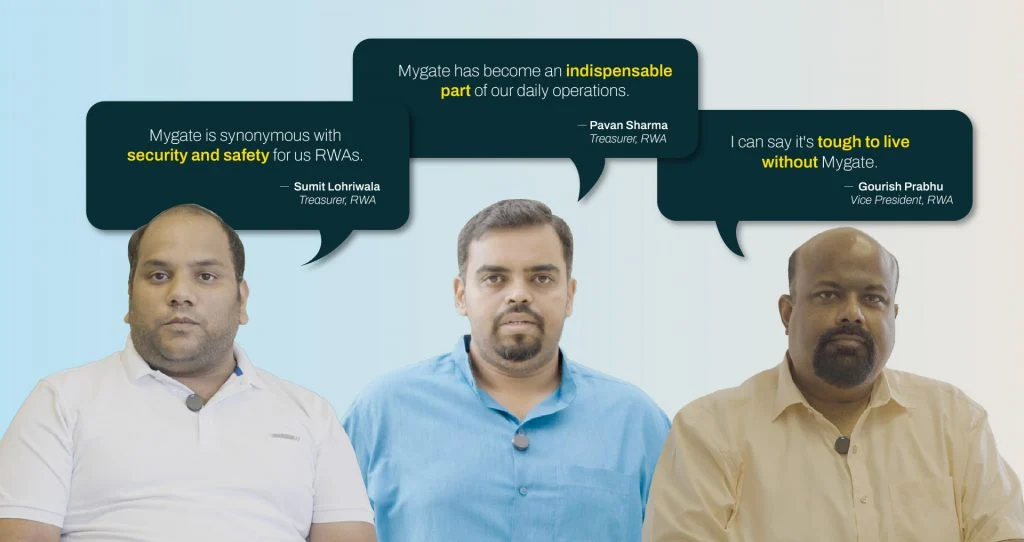

Loved by you, trusted by builders

Numbers reveal half of the tale, but actual RWA experiences tell even more. After implementing Mygate ERP, monthly collection accuracy increased by more than 60% in a luxury Mumbai township. Manual Excel work was replaced by automated billing and payment reminders, which eliminated missing dues and relieved committee members of their workload.

Helpdesk resolution time has decreased by 45% in many affluent Bangalore communities. Why? Maintenance requests were no longer lost in WhatsApp groups; instead, they were monitored centrally, with clear service level agreements and automated progress updates for residents.

Beyond individual success stories, entire communities have changed the way they operate. Our case studies demonstrate how RWAs across India have improved financial transparency, operational efficiency, and resident satisfaction.

Mygate’s ERP is more than simply a system; it is a smarter method to run a community, lowering accounting workload by 70% and making audits almost stress-free. RWA leaders frequently report increased collections, smoother budgeting, and a greater sense of control after switching.

[Explore our comprehensive case studies to see detailed transformations and measurable results from communities similar to yours.] https://mygate.com/community-management/success-stories/prestige-song-of-the-south/ and https://mygate.com/community-management/success-stories/elita-promenade/

Leading builders across India have standardized on Mygate for their premium developments. This isn’t just about convenience, it’s about providing consistent quality that residents expect in modern communities.

App store ratings consistently show Mygate ahead of competitors. Residents particularly praise reliability and responsive customer support when issues arise.

What the media says

Mygate’s remarkable journey has caught national attention. Business Today featured the inspiring story of Mygate’s founder, who left his Goldman Sachs position to work as a security guard, understanding ground-level challenges firsthand before building India’s leading community management platform. Read more

The Wire’s “Crafting Bharat” series highlighted CEO Abhishek Kumar’s vision of transforming gated communities through technology, showcasing how AWS partnership ensures 24/7 reliability for 4 million daily validations and Mygate’s evolution into a comprehensive living experience platform. Read more

Even critical perspectives from India Today acknowledge Mygate’s dominance in urban living, noting how the platform has become an essential part of residential life across Indian cities. Read more

Mygate’s ecosystem vision

Most community management platforms address issues in silos: billing in one app, helpdesk in another, and notices elsewhere. Mygate takes a more strategic, united approach.

It serves as a comprehensive ERP operating system for communal living, integrating finance, helpdesk, communication, and compliance. Billing communicates directly with collections and ledger entries. Vendor payments are recorded alongside TDS compliance and audit reports. Notices, polls, and AGM planning all flow effortlessly through a single dashboard.

Everything communicates data smartly. Outstanding dues have an impact on access control. Expense trends influence budgeting. Complaint history influences vendor performance evaluation.

This ERP environment lowers tool clutter, improves governance, and provides MCs with real-time information without requiring them to transfer platforms. When something breaks, whether it’s a pipe or a payment trail, you don’t waste time inspecting systems. It’s all there, interconnected and actionable.

FAQs

What makes Mygate better than other society apps in 2026?

Mygate offers much than just basic functionality; it is a full-fledged Society ERP. Everything, from invoicing and auditing to helpdesk and compliance, is connected. It is designed for scalability, transparency, and automation, making community management smarter and easier.

How future-ready is Mygate?

Mygate is designed as a scalable Society ERP, not just an app. Its modular architecture enables automation, integrations, and dynamic community demands, preparing it for smart homes, UPI mandates, GST upgrades, and whatever comes next.

Does Mygate provide better ROI for RWAs?

Yes, through faster issue resolution, reduced manpower requirements, and improved resident satisfaction. These improvements translate to measurable cost savings and better community operations.

What makes Mygate different from other society management apps?

Unlike others, Mygate is a complete society management software, not simply a set of functions. It combines billing, accounting, security, communication, and helpdesk into a one platform that provides automation, compliance, and control at scale.

Can Mygate reduce manpower dependency in society management?

Yes. Mygate automates critical activities such as invoicing, collections, complaint monitoring, and vendor payments to save manual effort and errors. With digital approvals, smart notifications, and real-time dashboards, RWAs may operate efficiently with a small staff.

Conclusion

Mygate began operations in Bengaluru in 2016, and by 2019, it has reached over 1,000 societies. Since then, it has had a significant impact, with 60% fewer unauthorised visitor incidents, 45% faster maintenance response, and top app store ratings. Mygate, trusted by India’s best builders, is the go-to choice for luxury communities.

More than an app, Mygate is a full-stack Society ERP that is ISO-certified, AES-encrypted, and designed to scale from small societies to mega-townships. With updates every 2-4 weeks, it evolves in response to customer needs, resulting in measurable cost reductions and efficient RWA governance.

Redevelopment is much more than a construction project; it’s a once-in-a-lifetime opportunity for your housing society to modernize living spaces, upgrade amenities, and add lasting value.

Over the years, policy shifts have made redevelopment more accessible and efficient. From the early changes in 2012 to the recent 2025 rules giving developers only two months to act, the landscape is evolving. But with opportunity comes responsibility: careful planning, informed decisions, and clear communication are essential for success.

Make sure everyone agrees on what matters most

The first step is uniting the society members around a common vision. Redevelopment affects everyone, so knowing what’s non-negotiable, whether it’s maintaining green spaces, ensuring parking adequacy, or safeguarding heritage features, helps avoid misunderstandings later.

When all members agree on their priorities upfront:

- It simplifies discussions with developers and vendors.

- It prevents surprises during project execution.

- It helps focus negotiations on what truly matters.

Skipping this step often leads to delays, disputes, and distrust. Remember, redevelopment isn’t just about buildings; it’s about community.

Focus on building for the future, not just bigger spaces

Redevelopment should envision the society’s future lifestyle, not just add floors or increase flat sizes. Think about:

- Creating green open spaces that encourage outdoor activities and improve air quality.

- Designing safe, step-free pathways and entrances that help senior citizens and differently-abled residents move around easily.

- Planning parking thoughtfully to prevent congestion and protect vehicles.

- Including community halls, play areas, and wellness spaces that support multi-generational living.

This future-focused approach increases society’s attractiveness and ensures the new development remains relevant and comfortable for decades.

Think about the costs that come after the construction is done

A modern building can come with unexpected expenses if long-term costs aren’t considered. Societies should factor in:

- Maintenance of eco-friendly features like solar panels and water recycling systems.

- Regular upkeep of green spaces keeps the environment healthy and appealing.

- Utility costs that might fluctuate due to design choices (for example, air conditioning requirements if ventilation isn’t optimized).

Working with developers who specialize in sustainable and cost-effective building designs can save society money and stress later.

Keep everyone updated at every stage of the process

Redevelopment projects span years and involve many moving parts. Keeping members well-informed reduces anxiety and builds trust. Societies should:

- Hire an independent Project Management Advisor (PMA) to ensure unbiased oversight on timelines, budgets, and quality.

- Consult legal experts early on to protect members’ rights and clarify contractual obligations.

- Provide regular updates and hold open forums for members to ask questions and voice concerns.

Transparent communication fosters a collaborative environment where all stakeholders feel valued and heard.

Look beyond the price when choosing a developer

While financial proposals matter, they shouldn’t be the sole criterion. When selecting a developer, consider:

- Their ability to finance the project fully, avoiding mid-way stalls.

- Track record in delivering projects on time and within budget.

- Reputation for quality, safety, and after-sales service.

- Past client references and feedback from other societies.

Doing thorough due diligence now helps avoid costly issues later.

Treat society funds with care and plan for the long term

Funds like hardship allowances or corpus money are precious resources. Instead of viewing them as easy cash, societies should:

- Use these funds strategically to cover redevelopment expenses and contingencies.

- Maintain meticulous records of expenditures for transparency and accountability.

- Make collective decisions about spending to ensure fairness and prevent misuse.

A disciplined approach to fund management ensures financial stability during and after redevelopment.

Remember, redevelopment is about renewing your community

Ultimately, redevelopment shapes the future of your community. When done thoughtfully, it brings modern comforts, strengthens bonds among residents, and enhances property value. It’s an investment not just in infrastructure but in the social fabric that holds your society together.

Take your time, involve everyone, pick partners carefully, and build a home that welcomes generations to come.

As real estate projects grow rapidly across Delhi, Resident Welfare Associations (RWAs) play an important role in ensuring transparency, compliance, and accountability within their communities. The Real Estate (Regulation and Development) Act, 2016, better known as RERA, has become the go-to framework for protecting homebuyers’ rights and regulating builders.

If you’re part of an RWA in Delhi, it’s crucial to understand the latest RERA guidelines and how they impact your community in 2026. This blog breaks down the essentials of Delhi RERA that RWAs should keep in mind, along with practical tips for using RERA effectively.

What is RERA & why does it matter to RWAs?

RERA was introduced to curb fraudulent practices by developers, reduce project delays, and ensure buyers get timely possession and quality homes. While it primarily governs builders and developers, RWAs have an indirect but critical role:

- They act as the voice of residents, ensuring builders stick to their promises.

- They help coordinate with developers for smooth handovers and defect resolutions.

- They assist residents in understanding their legal rights and options under RERA.

For RWAs, awareness of RERA guidelines helps protect residents’ interests and promotes healthier relationships between builders and residents.

Key Delhi RERA guidelines RWAs should know

1. Mandatory project registration:

Every builder must register any residential or commercial project with the Delhi RERA authority if it covers more than 500 square meters or has more than 8 units. This ensures projects are officially recorded and monitored.

- Registration details include project plans, approvals, timelines, and financial disclosures.

- RWAs should encourage residents to verify if their housing project is registered on the official Delhi RERA portal.

2. Project timelines & updates:

Developers are required to upload Quarterly Progress Reports (QPRs) showcasing construction progress, approvals received, and sales figures.

- This transparency lets RWAs and residents monitor if the project is on track.

- Delays must be reported, and completion certificates uploaded once ready.

3. Escrow account for fund management:

Builders must deposit 70% of the money collected from buyers into a dedicated escrow account linked to the project.

- This fund is strictly for construction and cannot be diverted.

- RWAs can use this information to reassure residents about proper fund utilization.

4. Agent registration & accountability:

Real estate agents representing a project must be registered with Delhi RERA and linked to that project.

- RWAs should ensure no unregistered agents are marketing properties within their societies to protect residents from fraud.

5. Complaint redressal mechanism:

RERA provides a platform for buyers to file complaints related to delays, quality issues, or misrepresentations.

- RWAs can assist residents in filing complaints using Forms M (general complaint) and N (adjudication) on the Delhi RERA portal.

- Complaints are usually resolved within 60 days.

How can RWAs leverage RERA for their communities?

1. Regular portal monitoring:

Assign a committee member to track your project’s status on the Delhi RERA portal every quarter. Check if:

- The builder has uploaded the latest QPR.

- The project status matches reality.

- The escrow account details are available.

2. Educate residents:

Host information sessions or circulate newsletters explaining what RERA means for homeowners and how to use the portal to check project details or file complaints.

3. Verify agents:

Institute society rules requiring all real estate agents to provide valid Delhi RERA registration numbers before entering the society. This prevents unauthorized and potentially fraudulent sales activities.

4. Collective complaint filing:

If your society detects builder violations, collaborate to file complaints as a group rather than individual residents. Collective action often speeds up resolution.

What about projects in ‘Abadi’ or ‘Lal Dora’ areas?

RERA regulations in Delhi have clarified that even projects in abadi or lal dora zones must register if they meet the area or unit count criteria. Many older housing societies fall under these zones, so it’s important to check whether your builder is compliant.

Challenges & limitations RWAs should be aware of

- Some smaller projects or individual builder plots may not come under RERA.

- RERA primarily deals with builders, so it won’t handle internal society disputes, but it can influence handover quality and timelines.

- Enforcement can be slow; patience and persistent follow-up are necessary.

Delhi RERA’s evolving rules aim to balance the scales between developers and buyers. For RWAs, understanding these rules means you’re not just passive observers you become informed advocates who can safeguard residents’ investments and push for timely project completion.

By regularly monitoring RERA updates, educating your members, verifying agents, and knowing how to file complaints, your society can wield RERA as a powerful tool to improve living standards and accountability.